All Categories

Featured

Table of Contents

This is regardless of whether the insured individual passes away on the day the plan begins or the day before the policy finishes. Simply put, the amount of cover is 'degree'. Legal & General Life Insurance Policy is an example of a degree term life insurance policy policy. A level term life insurance coverage plan can fit a variety of situations and requirements.

Your life insurance policy plan could likewise develop part of your estate, so could be based on Inheritance Tax read extra about life insurance policy and tax - Life insurance level term. Let's take a look at some attributes of Life insurance policy from Legal & General: Minimum age 18 Maximum age 77 (Life insurance policy), or 67 (with Crucial Disease Cover)

What life insurance coverage could you think about otherwise level term? Decreasing Life Insurance Coverage can aid protect a repayment home mortgage. The quantity you pay stays the very same, however the level of cover lowers about according to the way a settlement home loan lowers. Reducing life insurance policy can aid your loved ones remain in the family members home and stay clear of any additional interruption if you were to pass away.

If you choose level term life insurance policy, you can allocate your premiums due to the fact that they'll remain the very same throughout your term. Plus, you'll understand precisely just how much of a fatality advantage your recipients will get if you die, as this quantity won't change either. The prices for level term life insurance policy will certainly depend upon a number of variables, like your age, wellness standing, and the insurance coverage company you select.

When you go via the application and medical test, the life insurance coverage company will evaluate your application. Upon authorization, you can pay your initial premium and authorize any pertinent documents to guarantee you're covered.

What is Increasing Term Life Insurance? Pros, Cons, and Considerations?

You can pick a 10, 20, or 30 year term and delight in the included peace of mind you should have. Working with an agent can help you discover a policy that functions finest for your needs.

As you seek methods to safeguard your economic future, you have actually likely stumbled upon a wide range of life insurance policy alternatives. Picking the ideal insurance coverage is a large decision. You wish to discover something that will assist sustain your enjoyed ones or the causes important to you if something occurs to you.

What is Level Term Vs Decreasing Term Life Insurance Coverage?

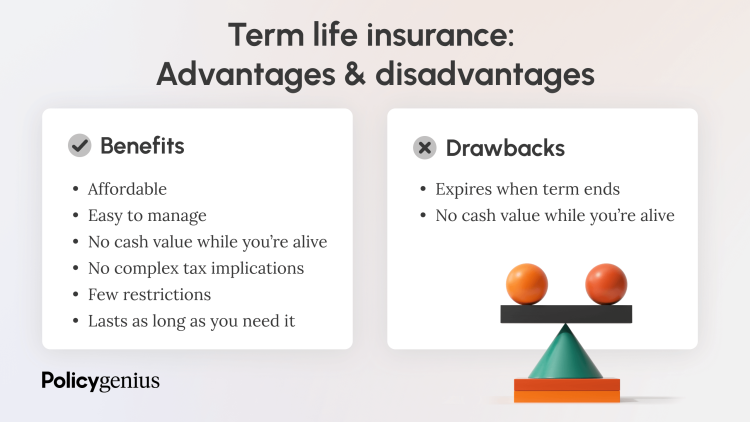

Lots of people favor term life insurance policy for its simpleness and cost-effectiveness. Term insurance policy agreements are for a relatively brief, specified amount of time however have options you can tailor to your needs. Certain advantage choices can make your costs change gradually. Level term insurance policy, however, is a type of term life insurance coverage that has regular payments and an unchanging.

Degree term life insurance policy is a part of It's called "level" because your premiums and the advantage to be paid to your enjoyed ones remain the same throughout the agreement. You won't see any adjustments in expense or be left questioning its value. Some agreements, such as yearly renewable term, might be structured with costs that raise gradually as the insured ages.

They're established at the start and stay the exact same. Having regular settlements can help you better plan and budget because they'll never ever change. Fixed death benefit. This is also evaluated the beginning, so you can understand precisely what death advantage quantity your can anticipate when you pass away, as long as you're covered and updated on premiums.

This often in between 10 and three decades. You accept a set premium and fatality benefit throughout of the term. If you die while covered, your survivor benefit will certainly be paid to loved ones (as long as your premiums depend on date). Your beneficiaries will recognize in advance of time just how much they'll obtain, which can assist for preparing purposes and bring them some monetary safety.

What is Level Term Life Insurance Meaning? Learn the Basics?

You might have the option to for one more term or, more likely, restore it year to year. If your agreement has actually an ensured renewability provision, you might not need to have a brand-new medical examination to keep your protection going. Nevertheless, your costs are likely to raise because they'll be based upon your age at revival time.

With this option, you can that will certainly last the rest of your life. In this situation, again, you might not need to have any brand-new medical examinations, however costs likely will rise because of your age and new coverage (Joint term life insurance). Various companies provide various alternatives for conversion, make sure to understand your choices before taking this step

Talking to an economic advisor likewise may assist you establish the course that aligns ideal with your overall strategy. The majority of term life insurance policy is level term for the duration of the contract period, yet not all. Some term insurance policy may include a premium that rises over time. With decreasing term life insurance policy, your survivor benefit goes down gradually (this kind is frequently secured to particularly cover a lasting financial obligation you're settling).

And if you're set up for eco-friendly term life, after that your premium likely will go up annually. If you're checking out term life insurance policy and desire to ensure uncomplicated and foreseeable financial defense for your family, degree term may be something to consider. Nonetheless, as with any type of protection, it may have some restrictions that don't fulfill your needs.

What is Short Term Life Insurance Coverage Like?

Commonly, term life insurance is much more economical than permanent insurance coverage, so it's a cost-effective way to protect economic protection. At the end of your agreement's term, you have multiple alternatives to proceed or relocate on from protection, commonly without requiring a clinical test.

As with various other kinds of term life insurance coverage, once the contract ends, you'll likely pay greater premiums for coverage due to the fact that it will recalculate at your existing age and health and wellness. If your financial circumstance adjustments, you might not have the needed coverage and could have to buy extra insurance coverage.

However that doesn't indicate it's a suitable for everyone (10-year level term life insurance). As you're purchasing life insurance policy, below are a couple of vital variables to consider: Budget. Among the advantages of level term protection is you recognize the cost and the fatality advantage upfront, making it simpler to without stressing about rises with time

Age and wellness. Generally, with life insurance policy, the healthier and more youthful you are, the even more economical the protection. If you're young and healthy, it might be an enticing option to secure in reduced costs currently. Financial responsibility. Your dependents and monetary responsibility play a role in determining your coverage. If you have a young family, for circumstances, degree term can aid provide financial backing throughout crucial years without spending for coverage much longer than essential.

{kind=link}

Latest Posts

Senior Care Usa Final Expense

Life And Burial Insurance

Final Expense Insurance Quote