All Categories

Featured

Table of Contents

That typically makes them a more budget-friendly choice for life insurance protection. Lots of people obtain life insurance policy protection to help economically shield their loved ones in situation of their unforeseen death.

Or you may have the choice to transform your existing term coverage into a permanent plan that lasts the remainder of your life. Various life insurance policies have possible advantages and downsides, so it's important to comprehend each before you choose to buy a policy.

As long as you pay the costs, your beneficiaries will certainly get the fatality advantage if you die while covered. That said, it is very important to keep in mind that a lot of plans are contestable for two years which means protection could be retracted on fatality, should a misstatement be located in the application. Plans that are not contestable often have a graded death advantage.

Premiums are generally reduced than entire life plans. You're not locked into an agreement for the rest of your life.

And you can not cash out your plan during its term, so you won't obtain any kind of financial take advantage of your past insurance coverage. Similar to other types of life insurance policy, the price of a level term plan relies on your age, coverage needs, work, way of life and wellness. Usually, you'll find much more budget friendly protection if you're younger, healthier and less high-risk to guarantee.

Dependable Level Premium Term Life Insurance Policies

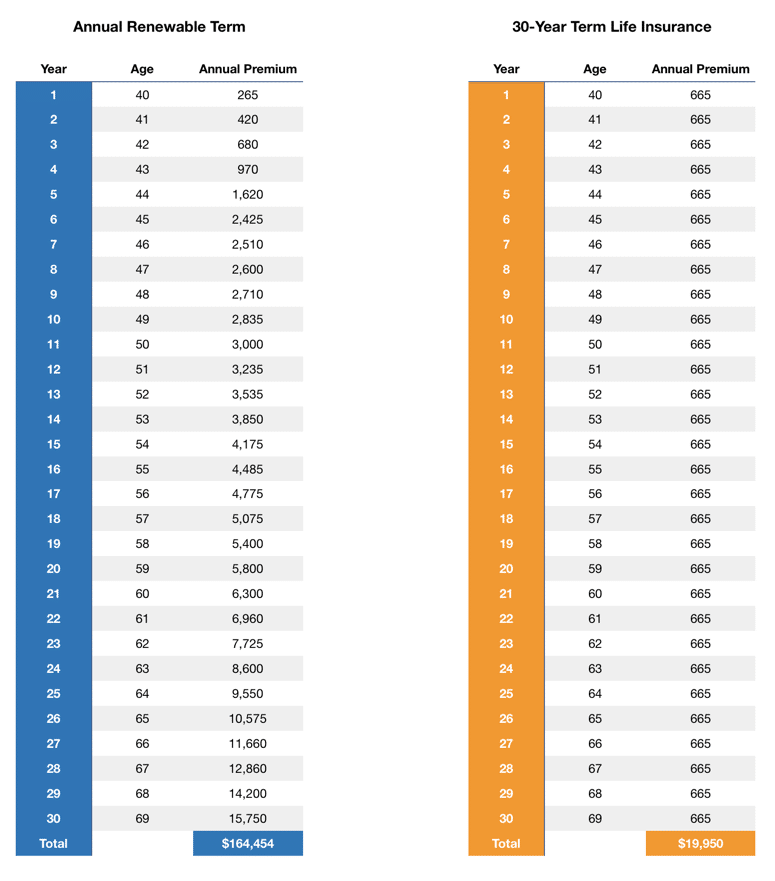

Considering that level term costs remain the same throughout of insurance coverage, you'll know exactly just how much you'll pay each time. That can be a large assistance when budgeting your expenses. Level term insurance coverage likewise has some adaptability, allowing you to personalize your policy with additional attributes. These usually can be found in the form of cyclists.

You might have to fulfill specific problems and qualifications for your insurer to pass this rider. There likewise might be an age or time limitation on the coverage.

The survivor benefit is normally smaller, and coverage generally lasts till your youngster turns 18 or 25. This biker may be a more cost-effective method to help guarantee your youngsters are covered as bikers can often cover numerous dependents at once. When your kid ages out of this coverage, it might be feasible to transform the biker right into a brand-new plan.

When comparing term versus long-term life insurance policy. term life insurance with accelerated death benefit, it is necessary to keep in mind there are a couple of different kinds. The most common kind of long-term life insurance is whole life insurance policy, but it has some crucial distinctions contrasted to level term coverage. Right here's a standard review of what to take into consideration when contrasting term vs.

Entire life insurance policy lasts forever, while term insurance coverage lasts for a specific period. The costs for term life insurance policy are generally less than whole life protection. Nevertheless, with both, the premiums remain the very same throughout of the plan. Whole life insurance policy has a cash worth component, where a part of the premium may grow tax-deferred for future demands.

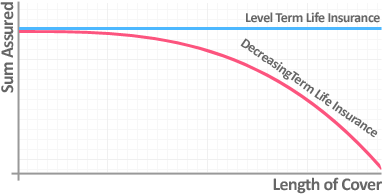

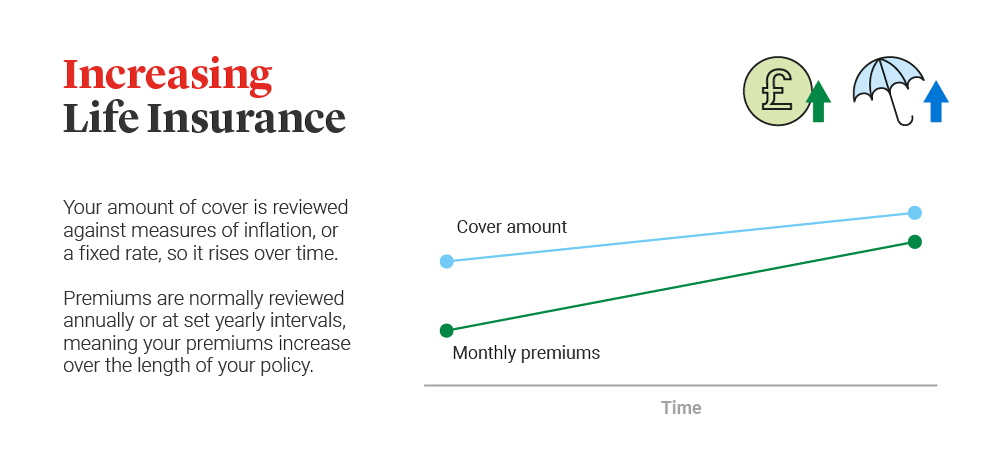

Among the major features of level term insurance coverage is that your costs and your fatality advantage don't change. With lowering term life insurance policy, your costs remain the very same; nevertheless, the survivor benefit amount gets smaller in time. For instance, you may have protection that begins with a survivor benefit of $10,000, which can cover a home mortgage, and then every year, the fatality benefit will reduce by a collection amount or percentage.

Because of this, it's frequently a much more affordable kind of degree term coverage. You may have life insurance policy through your company, however it may not suffice life insurance policy for your requirements. The primary step when acquiring a plan is establishing just how much life insurance policy you require. Consider elements such as: Age Family size and ages Work standing Earnings Financial debt Way of life Expected final costs A life insurance policy calculator can help establish just how much you need to start.

After picking a plan, complete the application. For the underwriting procedure, you might need to offer basic individual, health and wellness, lifestyle and employment information. Your insurance company will certainly figure out if you are insurable and the threat you might provide to them, which is reflected in your premium prices. If you're authorized, authorize the documents and pay your first costs.

Expert Joint Term Life Insurance

Consider scheduling time each year to assess your policy. You may wish to update your beneficiary information if you have actually had any considerable life adjustments, such as a marriage, birth or divorce. Life insurance coverage can often feel challenging. You don't have to go it alone. As you explore your alternatives, take into consideration discussing your demands, desires and worries about a financial specialist.

No, level term life insurance policy doesn't have money worth. Some life insurance coverage policies have an investment attribute that enables you to develop cash money worth gradually. A section of your premium repayments is established apart and can make interest in time, which expands tax-deferred throughout the life of your insurance coverage.

You have some options if you still want some life insurance coverage. You can: If you're 65 and your insurance coverage has run out, for example, you might desire to purchase a new 10-year level term life insurance policy.

Long-Term What Is Voluntary Term Life Insurance

You may have the ability to transform your term protection right into an entire life policy that will certainly last for the remainder of your life. Several kinds of level term plans are exchangeable. That indicates, at the end of your protection, you can transform some or every one of your plan to entire life coverage.

Degree term life insurance is a plan that lasts a collection term usually in between 10 and thirty years and features a degree survivor benefit and degree costs that stay the exact same for the whole time the policy is in effect. This means you'll understand specifically just how much your payments are and when you'll have to make them, allowing you to budget appropriately.

Level term can be a terrific alternative if you're looking to purchase life insurance policy coverage for the very first time. According to LIMRA's 2023 Insurance Measure Research Study, 30% of all adults in the U.S. need life insurance and don't have any kind of kind of policy yet. Degree term life is predictable and budget-friendly, which makes it among one of the most prominent types of life insurance.

{kind=link}

Latest Posts

Senior Care Usa Final Expense

Life And Burial Insurance

Final Expense Insurance Quote